Where to Build and How to Pay for It: Experts Weigh In

That we need more affordable housing—a lot more of it—is hardly in dispute. Attainable housing is the foundation of economic and social stability for American families, and by most estimates, the shortage of available, affordable homes in the US numbers in the millions.

And yet actually building more of the affordable housing that everyone seems to agree we need remains a challenge in communities across the country, as theoretical support crashes headlong into real-world resistance and constraints.

In a December webinar hosted by the Lincoln Institute of Land Policy, experts dove into the devilish details to address two of the thorniest questions that tend to haunt housing discussions: Where can we locate affordable housing? And how do we pay for it?

Mapping Public, Buildable Lots

In the first of two sessions, Jeff Allenby, director of geospatial innovation at the Lincoln Institute’s Center for Geospatial Solutions (CGS), shared how CGS is leveraging technology to help local policymakers get the data they need to act on housing.

“We’ve developed a unique, rapid, and robust method to unlock critical information about America’s housing stock,” Allenby said, describing Who Owns America, a unique analysis CGS developed to help local leaders understand and act on emerging issues like out-of-state investor ownership or locating underutilized lots in parcel-by-parcel detail. “It’s the same type of sophisticated insights the private sector uses to profit from residential housing, but instead we put these insights in the hands of policymakers so they can protect and preserve affordability.”

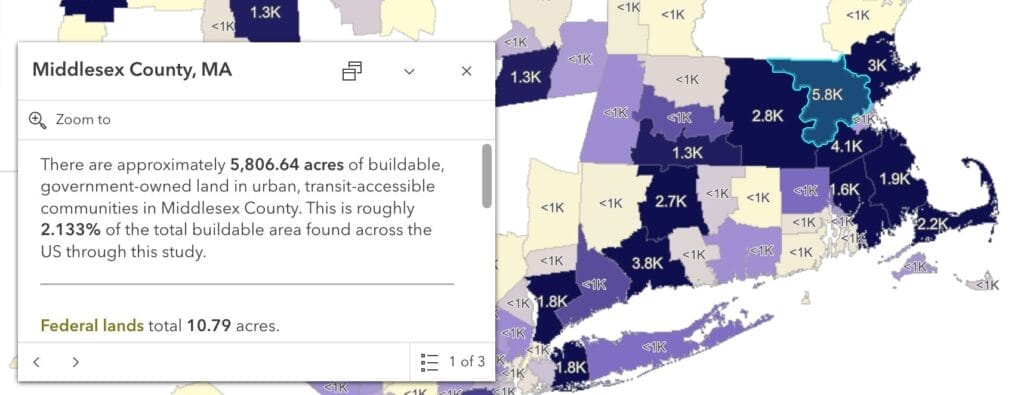

CGS cleans and standardizes parcel-level ownership data, fusing it “with authoritative sources like deed information, corporate structures, and census data to fill in gaps and paint a richer picture all in one place,” Allenby explained. “There’s never been such a severe shortage of homes in the United States,” Allenby said. “To address it, we need more housing—affordable housing—built close to where people work and where they want to live. But the big question we’re trying to answer is, where do we build it?” he added. “For us, the answer starts with data—building an inventory of available land in your area.”

Researchers and officials from across the political spectrum have expressed a growing interest in siting new housing on city- or government-owned property. That prompted CGS to evaluate all the government-owned lots across the country and their potential to support new housing, explained Reina Chano Murray, associate director at CGS. “We were curious: How much land is government owned, and how much of an impact can it truly have?” she said.

Murray demonstrated how the CGS team identified over 270,000 acres of buildable, transit-served lots owned by government agencies in major metro areas—enough acreage to support nearly two million homes at the relatively low density of seven units per acre. Most of that land, Murray noted—237,000 acres—is controlled by local governments, making them uniquely positioned to act. “Ultimately, the ability to turn these housing opportunities into reality rests with local policymakers,” she said.

The process began with identifying publicly owned land at all levels of government and scouring parcel records for keywords that would indicate government ownership, such as “Department of Transportation.” Many records are not so straightforward or standardized, though. Murray said her team has encountered “over 50 different ways to spell USA or United States of America, and the variations in naming conventions only increase” at the local level.

From there, the team winnowed the data further to include only census tracts in urban areas and economic centers — where the most housing demand exists — and further still, to areas within a quarter-mile of a transit stop with hourly service or better at rush hour. Murray’s team then removed parks and other green spaces, vital infrastructure, and public buildings, such as administrative offices, schools, community colleges, and hospitals.

To narrow it down to truly buildable lots, they excluded places located in flood hazard areas and chose parcels of at least 20,000 square feet where any existing structures occupied no more than 5 percent of the lot. “We now have a clear and data-backed answer that indicates significant opportunity for addressing the affordable housing crisis using government-owned land,” Murray said. “Our analysis identified over a quarter of a million acres of prime, development-ready land in transit-accessible, urban neighborhoods.”

Murray then presented findings from another inquiry. In response to so-called “YIGBY” laws (Yes In God’s Backyard) passed in California and Arizona—which make it easier for churches, temples, mosques, and other faith-based organizations to build housing on their properties—the Boston-based Lynch Foundation commissioned CGS to determine how much affordable housing could be built on land owned by faith-based organizations in Massachusetts.

After identifying about 7,000 properties owned by faith-based organizations statewide, a team of 15 students at Boston College “virtually visited” each site through a custom application, using Google Street View to examine each parcel and answering basic survey questions, such as whether there was developable space on-site or additional buildings not used for worship. CGS confirmed 1,973 faith-based parcels deemed to have over 203 million square feet of total developable space. At seven homes per acre, Murray said, “That’s enough land to build over 140,000 units of affordable housing in Massachusetts alone.”

The effort took less than two months to complete, from start to finish—showing plenty of potential for religious institutions to alleviate the housing shortage and for technology to help policymakers quickly and accurately identify buildable land that has been hiding in plain sight.

Funding the Future

If locating land is the first step, finding the financing to build housing on those lots is the next challenge. Lincoln Institute Senior Fellow R.J. McGrail welcomed three partners affiliated with Lincoln’s Accelerating Community Investment (ACI) initiative to discuss funding strategies for affordable housing development.

Laura Brunner, president and CEO of the Port of Greater Cincinnati Development Authority, kicked things off on a positive note. She explained how Cincinnati, like other Midwestern cities, has been a prime target for institutional investors whose playbook involves outbidding first-time buyers to purchase single-family homes, then renting them out, often at inflated rates, locking residents out of homeownership opportunities.

But in 2022, the Port learned about a portfolio of almost 200 investor-owned rental houses that were being auctioned out of receivership. With a goal of restoring homeownership opportunities for the city’s low- and middle-income residents, the Port issued both taxable and tax-exempt bonds to enter a $15.5 million bid on the portfolio—and won.

“We first went to our nonprofit partners to ask if they would support us, and what we heard back was, ‘Yes, you have a mandate, a moral imperative to do this. We have to save these homeownership opportunities,’” Brunner said.

The plan was to rehab the vacant homes and sell them at prices affordable to buyers earning 80 percent of the area median income (AMI), while stabilizing the existing tenants and getting them prepared for eventual homeownership through home-buying education and financial counseling.

“We issued these bonds really confident that we were going to be able to take 200 homes and put them back into homeownership from rental without any subsidy, which is unheard of—all the new home construction we do requires a significant amount of subsidy,” Brunner said.

But while the receiver had claimed 10 of the properties were vacant, at least 60 of them turned out to be unoccupied—and in very bad shape. The Port has thus spent more money than expected to get the vacant houses ready for resale (and, at a local appraiser’s suggestion, to perform essential upgrades that most low-income homebuyers can’t afford to do themselves, like installing air conditioning). “When we found out the condition the houses really were in, we did need subsidy,” Brunner said. “But we’ve been successful . . . raising a number of grants that allow us to continue to keep the price down as much as possible.”

To date the Port has rehabbed and sold half of the 60 vacant homes at an average price of $150,000. “These are low- and moderate-income Black and brown neighborhoods [where residents] have basically not had an opportunity to purchase a home because such a high percentage were owned by these investors, and so we’re suppressing the sales price as much as we can,” she said.

The Port, which has also created affordable housing through a local land bank it’s managed since 2011, requires homebuyers to occupy its homes for at least five years before reselling. And after more than a decade of doing so, their efforts are creating real neighborhood wealth, Brunner said.

“We’ve done it long enough now that we’ve had about 30 people that have subsequently sold their house, and what we found is that those homeowners had a profit of 52 percent,” Brunner said. “So it proves that, even in these deeply distressed neighborhoods, we are making a market and . . . there’s wealth creation opportunity, which is what we’re all about.”

Plugging Gaps with Flexible Funding

MassHousing, the state housing finance agency for Massachusetts, also views homeownership as a way to help close the racial wealth gap, said Executive Director Chrystal Kornegay. “We sell tax-exempt and taxable bonds and use the proceeds of those bonds to lend to low- and moderate-income homebuyers,” she explained, as well as to developers of rental housing to ensure they keep a portion of their units affordable.

But when MassHousing conducted a study on where people of color were buying homes in Massachusetts, the organization noticed a pattern: Not only was new housing not being built at the pace it was two decades ago, Kornegay said, “but where it was being built was not the places in which people of color lived.” In response, the agency is trying to ensure some of its programs, such as down payment assistance for first-time buyers and incentives for affordable housing developers, are used more often in communities where people of color want to live.

Kornegay then discussed how zoning is often perceived as the primary obstacle to getting more affordable housing built but said that financing has become an even bigger hurdle in recent years, due to higher interest rates and other market conditions.

“Getting access to capital has become a huge barrier,” she said, noting that over 20,000 already-permitted units in Massachusetts have stalled out in development “because the capital stack for those deals just didn’t make sense anymore.”

Most large-scale, multifamily buildings in Massachusetts are permitted through the state’s comprehensive permit law, known as 40B, Kornegay said. And since those projects require at least 20 percent of the units to be affordable, at 80 percent of AMI, “they have affordability built into them,” she said. So Massachusetts created a flexible financial product geared specifically toward such projects, available through MassHousing, called “Momentum Equity.” While not a subsidy, it’s designed to blend with private financing and inject the extra capital needed—up to 25 percent of a project’s equity—to get more of those developments off the sidelines and into production. (Equity financing refers to an investment-style ownership stake, as opposed to a loan that is paid back at agreed-upon terms.)

A second new product, which can be paired with Momentum Equity funding, is called the FORGE loan. “We’ve created this product along with Freddie Mac, in which MassHousing as a lender would put up 10 percent of the total loan amount and serve in the first loan-loss position,” Kornegay explained, thereby securing more favorable lending terms. “These products together really can make an impact in the capital stack and get a bunch of units into construction in the next six to 12 months.”

Tapping Federal Funds Outside of HUD

Greg Heller, director of housing and community solutions at the global consulting firm Guidehouse, described how the two major pandemic relief acts passed by Congress provided a huge influx of federal money that could be used for housing over the past few years—and how more funding exists, if communities know where and how to look for it (and if the funds survive possible freezes or cuts enacted by the Trump administration).

Federal pandemic relief funding provided “new sources of capital that could be applied for things like eviction prevention programs, for things like housing and counseling, and first and foremost for gap financing for either tax-credit projects or non-tax-credit projects,” he said. “Everybody all over the country was trying to figure out how to harness and use these new financing sources.” About 10 percent of the $350 billion that cities and counties received in local recovery funds through the American Rescue Plan Act (ARPA) went to housing, he added—money that needs to be spent by 2026.

What’s interesting, Heller added, is that none of that money came through the Department of Housing and Urban Development (HUD). “Obviously, HUD continues to play a leading role . . . but all of these sources came through Treasury, and Treasury started to play a significant role in creating guidance around these programs and understanding how to blend and braid and layer this financing with conventional HUD entitlement sources.”

With ARPA funds hitting their obligation deadlines in 2026, Heller said, “the question is what comes next? And the answer is the funds in the Inflation Reduction Act.”

While ARPA funds were very flexible and could be used for a broad range of activities, he said, the IRA funds are funneled through specific programs at different agencies, including the US Department of Energy, the Environmental Protection Agency, and the Treasury, as well as HUD.

“They all have different program guidelines, they all have different definitions of things like low-income disadvantaged communities, and so again it falls on cities, states, counties, to figure out how to harness these programs and use them to fill capital gaps for affordable housing, because it’s one-time funding,” he said. But the scale of the funding makes it worth wrestling with the complexity of the programs, he added.

The EPA, for example, has made $27 billion in funding available through three sources: the $7 billion Solar for All program, the $6 billion Clean Communities Investment Accelerator, and the $14 billion National Clean Investment Fund. “The latter two are flowing through awardees which are coalitions of green banks and CDFIs who are developing their product and starting to close loans and get those funds out on the street, and a lot of that is going to affordable housing,” he said.

The Solar for All program works through designated state entities and regional nonprofits, who aren’t as accustomed to housing finance. But Guidehouse has been working with state housing finance agencies to find ways to also tap into these funds, which can be used to help cover costs associated with rooftop solar installations and building electrification, for example.

“There’s a huge opportunity, for not just financing [on-site] energy generation, but also a range of other costs within the projects to get them solar-ready,” he said. “So those are tremendous opportunities for gap financing for affordable housing projects.”

Heller also urged attendees not to overlook home energy rebates from the Department of Energy, even if they’re more commonly associated with single-family homeowners who want to install a heat pump or insulate their attic, for example.

“These are actually huge opportunities for financing affordable multifamily [housing],” he said. “It’s $8.8 billion, and 10 percent of every state’s rebate assistance has to go to low-income multifamily . . . so there’s a huge focus on low-income multifamily, and there’s categorical eligibility for a whole range of subsidized affordable housing programs, including LIHTC, public housing, HUD and FHA multifamily programs, and a variety of others.”

“Then finally there are a range of tax credit programs that were amended through the IRA to make them more flexible and more available for affordable multifamily projects,” he said.

Of course, Heller acknowledged, some of those programs could see cuts or changes in the Trump administration. “There’s uncertainty [about] how that’s going to impact the programs and their guidance and availability moving forward, and I don’t think anybody has the answer on all of that quite yet,” he said. But the administration has shown an interest in financing more affordable housing, so there could be new opportunities as well, he added. “There will continue to be new programs that everyone has to sort of, in real time, figure out how to pivot and harness those funds and get them into projects that need them.”

Where There’s a Way, There’s a Will?

Wrapping up the webinar, Lincoln Institute President and CEO George W. McCarthy reflected on how a huge national challenge—such as building an extra million homes per year on top of the 1.4 million a year we’re already constructing—can feel unassailable. “[And yet] we produced 2.4 million units of housing in 1972—a much smaller economy, a much smaller population,” McCarthy noted. “So it’s not that we can’t do it.”

As the presenters made clear, he said, buildable lots and funding options do exist—it’s a matter of showing people how to put the pieces together. “We have CGS ready to map it out for you, we have R.J. ready to show people how to blend public, private, and civic capital,” he said. “If we have the money, we have the land, we have the financing, what is missing? And what’s missing, of course, is the political will.”

And even that may not be the immovable obstacle it once was. Citing 12 states from across the political spectrum that have stepped in to preempt local zoning “to make sure that it’s possible to build housing where people have been preventing it from being built,” McCarthy said, “it’s not as if we don’t have some kind of bipartisan support for taking this on.”

With the land, money, and knowledge necessary to address our housing shortage, McCarthy concluded, “we just have to summon the real political will to get it done—and that’s a less daunting task than people would have you believe.”

Jon Gorey is a staff writer at the Lincoln Institute of Land Policy.

Lead image: The Boston Housing Authority’s Old Colony redevelopment project has used federal funding to convert distressed public housing into safe, affordable, energy-efficient rental units. Credit: Andy Ryan Photography via BHA.