The National Association for County Community and Economic Development (NACCED) will host its 50th Annual Educational Conference and Training in Mesa, Arizona, September 8–11, 2025. NACCED is a supporting organization of the National Association of Counties (NACo), which focuses on the county community and economic development profession.

The Lincoln Institute and Claremont Lincoln University will host a booth during the conference, where attendees will be able to see publications and resources, learn about scholarship opportunities for new degree and certificate students, and get more information about the Lincoln Vibrant Communities program.

On September 10, Lincoln Institute President and CEO George McCarthy will give the keynote speech for the conference, titled “Reclaiming Land, Rebuilding Trust: Who Owns the Land and Housing in America’s Counties? Should We Care?” In his address, he will highlight the shift in land and housing ownership happening across the US and will introduce Who Owns America—an innovative tool tracking landownership at the parcel level.

In Denver, Mike Johnston Confronts Success: The City’s Popularity Has Made It Pricey

July 9, 2025

SHARE

Listen on:

Denver Mayor Mike Johnston speaks with people at a homeless encampment. Johnston has made ending homelessness a goal of his administration. Credit: Denver Mayor's Office.

Mike Johnston, a one-time high school English teacher, has been overseeing a significant boom in one of the most prominent cities in the Intermountain West. Denver has been attracting people and businesses with its temperate climate and outdoorsy quality of life, but this popularity has also caused growing pains, starting with increasingly high housing costs, homelessness, and recently some significant municipal budget woes.

Johnston has tackled the challenges one by one, beginning with a permitting process overhaul, steps to reduce costs in building, and tax abatements and other incentives, like a density bonus, to encourage more construction.

“We have a lot of people that want to move to Denver. That’s driving a lot of economic growth. We’re thrilled about it. It also drives lots of housing demand,” Johnston said in an interview for the Mayor’s Desk series, recorded on the Land Matters podcast. “The overarching theme is, we have to add a lot more housing supply.”

In the wide-ranging interview, Johnston also reflected on his aggressive campaign to clear out homeless encampments in the city. As part of this effort, officials have provided customized relocations to private transitional housing units with services and support for the unhoused.

“When you have high cost of housing cities, you get more people who can’t afford to pay that cost. That is just a mathematical fact. And so that means many of the cities that are growing and are in high demand, like the Denvers, or the San Franciscos, or the Austins, or Seattles, are the places where we see this struggle.”

The strategy of individualized housing solutions, while expensive, has been working, he said. “We think it can work for other cities, and we’ll share these lessons with anyone who’s willing to take them on, because we think we should set the expectation in every American city that street homelessness can be a solvable problem.”

He also expressed confidence that the state and the metropolitan region will have continued success fighting climate change, as federal policy backs away from addressing that global crisis. He said incentives for electrification, electric vehicle infrastructure, and energy-efficiency upgrades like heat pumps are contributing to the city’s goal of being carbon neutral by 2040.

“We don’t want to make it too expensive to do business in Denver, and yet we still want to be aggressively committed to hitting climate goals,” he said. “People do care. And there’s a lot we can do,” such as encouraging residents to take more trips by bike or walking, or to consolidate trips made in single occupancy vehicles.

“We want to encourage people to take more local action now, in the face of federal abandonment of [climate action] … we’ll keep setting our own targets for how our vehicles, our businesses, and our residents try to hit aggressive climate goals, knowing that we’re still all in this together, even if the President doesn’t want to make it a priority.”

Being mayor is the latest step in a professional journey that began with teaching English in the Mississippi Delta. From there, Johnston returned to Colorado to become a school principal, leading three different schools in the Denver Metro area. In 2009 he was elected to the Colorado State Senate, where he served two terms representing Northeast Denver. He was also a senior education advisor to President Obama and CEO of Gary Community Ventures, a philanthropic organization, where he led coalitions to pass the state’s first plan for universal preschool and spearheaded efforts to fund affordable housing and address homelessness statewide. He lives in East Denver with his wife Courtney, who is a chief deputy district attorney, and their three children.

Johnston, 50, was part of the Lincoln Institute mayor’s panel at the American Planning Association’s National Planning Conference in Denver this spring, along with Aaron Brockett and Jeni Arndt, mayors of the Colorado cities of Boulder and Fort Collins, respectively. Senior Fellow Anthony Flint caught up with him several weeks later for this interview, which will also be available in print and online in Land Lines magazine.

Anthony Flint is a senior fellow at the Lincoln Institute of Land Policy, host of the Land Matters podcast, and a contributing editor of Land Lines.

Transcript

Anthony Flint: Welcome back to land matters, the podcast of the Lincoln Institute of Land Policy. I’m your host, Anthony Flint. On this show, we’re continuing our Mayor’s Desk series –- our Q&A’s with municipal chief executives from around the world — with Denver Mayor Mike Johnston, who was inaugurated as the 46th mayor of that city pretty much 2 years ago this summer in July 2023. It’s fair to say he’s been overseeing a significant boom in one of the most prominent cities in the Intermountain West, which has been attracting people and business with its temperate climate and outdoorsy quality of life. Yet Denver has had its growing pains, too, with increasingly high housing costs. We see modest bungalows in several neighborhoods in Denver, easily selling for a million dollars or more … a not-unrelated homelessness problem, and recently some significant municipal budget woes.

Mayor Johnson started his career as a high school English teacher in the Mississippi Delta, and returned home to Colorado to become a school principal, leading 3 different schools in the Denver Metro area. He later served as a senior education advisor to President Obama. In 2009 he was elected to the Colorado State Senate, where he served 2 terms representing Northeast Denver, working on issues, including immigration, gun safety and the clean energy transition. He later served as the CEO of Gary Community Ventures, a local philanthropic organization where he led coalitions to pass the State’s 1st plan for universal preschool and spearheaded efforts to fund affordable housing and address homelessness statewide. Mayor Johnston grew up in Colorado, speaks Spanish and lives in East Denver with his wife Courtney, who is a chief deputy district attorney and their 3 kids. Your honor, thank you for joining the conversation at Land Matters, and being part of the Mayor’s Desk series.

Mayor Mike Johnston: I’m delighted to be on. Thank you so much for having me.

Anthony Flint: Well, as I mentioned in the intro, like a lot of booming metropolitan regions, Denver is facing down a housing affordability problem. So, first question, what are the key elements for addressing this crisis?

Mayor Mike Johnston: You bet, Anthony, and again thank you for having me, and I think the opening frame for me which you mentioned … My dad used to say, the only thing worse than being hated is being loved, you know, and what we know for Denver is, we do have folks from all over the country and all over the world who want to move to Denver. And that is a great problem to have. I have friends who are mayors and cities facing very different challenges, which is declining populations and lots of vacant buildings, because people don’t want to move there. Denver is now, I think, the number 2 desired destination for people under age 30 in the United States. And so we have a lot of people that want to move to Denver. That’s driving a lot of economic growth. We’re thrilled about it. It also drives lots of housing demand.

So for us there are three big top priorities here. The overarching theme is, we have to add a lot more housing supply, as you know, but we think there are three ways to do that. One is to make it faster to build housing for us. That means an aggressive strategy on permitting reform to make our permitting system go from what was a two and a half to three-year process to now, what will be a commitment from us to have every permit only take 180 days of time in the city’s hands. We created a new citywide permitting office that unifies all of the functions of permitting that were spread across seven departments, now into one director, who reports directly to me so part of that is making it easier to build in Denver.

The second is reducing the costs of building wherever we can. And so we’re doing that, obviously making the process faster. Reduce the cost. But also we’re doing more to provide our own tax abatements and our own tax programs. We launched a middle class housing strategy this week. That’s focused on providing property tax abatements for up to 10 years in exchange for a 30 year, commitment on deed, restricted affordability for people that are middle class Denverites who need to be able to afford to live in the city. So we think those incentives matter. And then, of course, we are investing more in affordable housing. We know that the city can’t solve this alone, and the market can’t solve it alone. We need a partnership where we will invest city resources into projects where we can be hopefully a smaller and smaller part of the capital stack. But just enough of the stack to be able to buy long-term affordability in the form of deed restrictions. And so for us, it’s making the city build faster. It’s making costs cheaper. And it’s making more public investment with really clear public goals. We’ve set a clear public goal to bring on 3,000 affordable units every year, and provide access for 3,000 households to affordable units every year. That’s about twice the rate what the city was bringing on before we got into office. And so we know we have to be really aggressive about bringing on a lot more housing, a lot more quickly and a lot more affordably.

Anthony Flint: Your campaign to address homeless encampments in Denver triggered a little bit of backlash, including some criticism of the expense. Can you explain your approach, and how it might apply to other cities? And is there anything you would do differently?

Mayor Mike Johnston: Yeah, I think this is one that we are really excited about, because I think many Americans have given into the belief that homelessness is an unsolvable problem that we are just stuck with this as a component of modern life. And, as you said accurately, Anthony, what we know is homelessness exists in the greatest acuity in cities, not because there’s high rates of poverty, not because there’s high rates of unemployment, not because of the political ideology of those cities. It exists in direct correlation to the cost of housing. In those cities. When you have high cost of housing cities, you get more people who can’t afford to pay that cost. That is just a mathematical fact. And so that means many of the cities that are growing and are in high demand, like the Denver’s, or the San Francisco’s, or the Austins, or Seattle’s, are the places where we see this struggle. But what we have really seen is that this is a problem that can be solved by addressing those core needs. And so I’ll lead with the headline that … we set an ambitious goal to try to end street homelessness in my 1st term. Four years. That seems impossible. Well, I’ll tell you, we’re two years in right now, and we have now reduced our street homelessness in Denver by 45% in a little less than two years. That is … the largest reduction of street homelessness in any city in American history, over two years, of which we’re very proud. But it’s also a clear sign that halfway through the term. We’re halfway on the path of that goal. We think other cities should be ambitious. And believing that this is a solvable problem, let me talk about the way we’ve done this, which we think is also really scalable.

What we’ve done is first really focused on bringing on what we call transitional housing units which are dignified, individual private units. A lot of these are hotels we’ve bought and converted. They’re tiny home villages that we’ve built. But critically, it’s not shelter like sleeping on a gym floor with 100 people on a mat. It is a place where you have a locked door. You have privacy, you have access to showers and bathrooms and kitchens. You can store your stuff when you go to work for the day.

And we brought on wraparound services on each of these sites. So our first big effort was to bring on 1,000 units of transitional housing, you know, like many cities, previous Administration fought this battle, and took 2 or 3 years to fight, to put one tiny home village of about 40 units into one neighborhood with a number of lawsuits. We said, we have to bring on units at the scale of the problems. We brought on a thousand units, and (over) six months I did 60 town halls all across the city, talking to neighbors and all of those locations about why this would make such a big difference. We put wraparound services — mental health addiction, support, workforce training, long-term housing navigation — on each of those sites. So people don’t have to always return just to downtown to get those services. And once we brought those units on, then we went geographically to the places where encampments existed in Denver, and instead of sweeping those encampments from block to block, where they just show up in front of someone else’s house or someone else’s church or hospital, we would actually go to those encampments and resolve them. We would close that encampment entirely by moving all 50 people or 100 people. In one case we had almost 200 people in one encampment, closing those encampments, resolving them, moving all those folks into housing, and then importantly keeping that block or that region of the city permanently closed to future camping. So the result is, two years in, we’ve now closed every encampment in the city. We haven’t had a single tent inside of our downtown business district for more than a year and a half we have cut family homelessness by 83%. We’ve become the largest city ever to end street homelessness for veterans. We have no veterans anymore on the streets who can’t get access to housing, and, importantly, anyone can walk down any street or sidewalk or public park, and none of them have tents or encampments in them, so we’ve both made sure there’s a real change in the experience for residents of Denver and those people who are most at risk of starving to death, freezing to death, overdosing on the streets … we moved off of the streets into transitional housing that has really worked for us. We think it can work for other cities, and we’ll share these lessons with anyone who’s willing to take them on, because we think we should set the expectation in every American city that street homelessness can be a solvable problem.

Anthony Flint: Are you satisfied with the number of people using this very impressive and extensive light rail network in Denver Metro, and the number of people living essentially in transit oriented development? Or is the system facing growing pains, and if so, why? A related question … any lessons learned from the relatively light ridership on the free bus on the 16th Street Transit Mall, which is finally concluding its renovation after long delays? But first the light rail network, transit-oriented development … How is it going.

Mayor Mike Johnston: As you, said, Anthony, we’re not satisfied yet, and that is because, as you know, transit and housing have to be connected strategies. Housing is a transit strategy. If you’re mindful about actually building housing and building density of housing around our public transit networks. And so we had this great transit network built. We did not have density of housing around any of those spots. And so what we’re doing now is undertaking a series of very large catalytic investments in a number of areas around the city that are on these light rail lines. So we can build thousands and thousands of units of housing along that corridor. We just, for instance, acquired the largest piece of private property in city history to turn into a public park. It will be a 155-acre park. It is right next to a light rail stop, so we can now add housing and housing density all around that site — beautiful location, and people can get on light rail and get right to downtown or do a Broncos game or anything else. We just won a franchise expansion, the one franchise expansion for the National Women’s Soccer League, and so we’ll have a new women’s soccer franchise. We’re building a new women’s soccer stadium also at a TOD site that we’ll have on that campus … a lot of dense housing commercial activities also connected to public transit. We’re rebuilding our stock show in a historically Latino part of North Denver — Globeville, Elyria, Swansea — that’ll allow us to add about 60 acres of new housing, public spaces, commercial activation also all on public transit. So our belief is, you have to actually be deliberate about building real density around your public transit as much as you want to build your public transit around well traveled lines of travel in the city. And so that’s a big part of our strategy. When we add that density, we know most of the major cities like ours that aren’t yet a New York, or a DC, with a full functioning subway line. You can’t just throw in that infrastructure and hope the city accommodates because people have lots of places to go to. You have to build nodes of real density around the city. So even though you might have 3 or 4 different jobs over the next 10 years, those jobs can be concentrated among different regions, and your housing can, and your activities can (as well). So that’s our big strategy around that. And you’ll see us make historic investments in doing that in the next couple of years.

But a part of that is downtown, is our downtown strategy. And you mentioned our 16th Street bus that we have, that’s free downtown. We’re making the largest investment in our downtown, also of any city in the country, per capita. Right now, about $600 million through a tax increment financing system that will focus on one getting more people to live downtown. We want downtown to be a neighborhood, not just a business district. And so we’re going to add about 4,000 units of housing in our city center, using these funds that we have from our downtown Denver authority, because we know that means more people that will use that bus every day that we’ll get to and from work they will go to see friends. So that’s a big part of our strategy. We’re working on filling up about 7 million square feet of vacant office space — like many cities, have about 4 million of that, we will use with residential conversion. We think one of the most ambitious residential conversion plans in the country. The other 3 million we’ll use by bringing people back to the office, recruiting businesses to come downtown, stay downtown, we think the more we activate that location the more folks will use the public transit, and the more people can use the connected public transit of coming from a neighborhood in East Denver or North Denver, take the light rail down to downtown, use the 16th Street ride to get up and down 16th Street … we have the second largest theater complex in the country off of Broadway. We have 5 professional sports franchises in our city center. We have Michelin Star restaurants. We’ll have the Sundance film festival coming to Colorado. There’s so much to be attracted to seeing. We want to make it easy to get to downtown and around downtown, and this will do that.

Anthony Flint: Given the current municipal fiscal challenges in Denver, what is your thinking about alternative financing systems such as a land value tax or value capture, as seen in the 38th & Blake incentive overlay? I’m hoping you might explain the concept as you see it and how or whether its rationale makes sense to you.

Mayor Mike Johnston: We are interested in every incentive we can find to encourage folks to build more housing. The 38th and Blake overlay was really kind of a density bonus, where we allow folks to build higher buildings than what the zoning might allow in exchange for adding more affordable housing, and we are always looking at ways to incentivize folks to add more affordable housing. So we’re delighted to do that. I think that also links to the program I described briefly which is our our middle class housing program we launched yesterday, which is also focused on a property tax abatement. We’ll offer up to 10 years of property tax abatement for people that are going to build middle class affordable housing. So think about that as people making sixty to a hundred thousand a year as an individual … and that’s about a 10 year property tax abatement for a 30-year commitment of affordability. So that’s a great deal for us. We’re also looking at partnership on places where we have public land. We’re looking at working with city-owned land, working with Denver public schools where they have land, our regional transit system, if they have land. And so we’re always looking to contribute public land as a way to incentivize more affordability. But we want to do a all of the above strategy. But wherever we can add more housing without having to invest more dollars in these fiscal times that’s a big help

[Re-stated] Our belief is we want to do an all of the above strategy on every way we can incentivize people to build more affordable housing. So for us, that means we want to use city land. Whenever we can do that, we’ll use public land to be able to incentivize a deal. We’ll partner with other public agencies like the Denver public schools, or like the regional transit system or the State. That’s always a great way for us to incentivize. And that’s why we’ve used strategies like this middle class housing program we launched, which is a property tax abatement where folks can get 10 years of property tax abatement for a 30 year, commitment of deed, restricted affordability through a special limited partnership. So we’re going to use every strategy we have, particularly in tough economic times, and you don’t have big new dollars to invest in supporting affordable housing. We have to find other creative ways and density. Bonuses are a great way, and we’ll keep doing that as well as everything else we can.

Anthony Flint: Finally, how would you assess the progress of your climate action plans which I see includes incentives for electrification, electric vehicle infrastructure, hot and cold weather heat pumps, energy efficiency … Do you see a tangible embrace at the local level for addressing climate change, especially in the context of retrenchment at the federal level. I mean, just as a practical matter, the federal government is getting out of the climate business. So can cities and states take that over and be effective?

Mayor Mike Johnston: We don’t see any change at all in our city’s commitment to climate action or our conviction that this is a still existentially important effort for us to undertake. And so we are not slowing down at all. We’re not changing our path, and what we are doing is trying to make sure we’re committed to an aggressive vision to meet our climate goals, which for us is a 2040 plan to be entirely carbon free by 2040, to have 100% renewable energy. And also to make sure we’re driving economic growth. We want to do both. And so we don’t want to make it too expensive to do business in Denver, and yet we still want to be aggressively committed to hitting climate goals. And we’re doing that. We’ve done things like we had, I think, one of the nation-leading efforts on making our commercial buildings more energy efficient through a program we have called Energize Denver. We also had concerns from the business community about how to comply with the cost to make those adjustments to buildings. And so we spent a lot of time with our landowners and building owners and business leaders, and we revised that plan to both decrease the penalties, extend the amount of time folks can comply, put a cap on the overall amount of changes they have to make, which drops the cost dramatically for our business partners, but still keeps us on path to hit aggressive 2040 climate goals. So people do care. And there’s a lot we can do. There’s behavior change. We’re doing a whole campaign on behavior change, to encourage folks to take more trips by bike or walking … Can they consolidate or condense the number of single occupancy vehicle trips that they take. And so part of it is about awareness. Part of it’s about behavior change and part of it’s about a good policy on things like banning plastic bags. Obviously, and being able to incentivize more and more solar and wind. So we think this is purely a part of Denver’s brand. We want to be able to be a great city and a good city. We want to be able to have a great economy, and also have great connection to the natural environment of the outdoors. And so for us, it’s it’s good climate and good business, and we’ll continue to do both.

Anthony Flint: And local and state government taking this over, are you optimistic about that? The question is, can they really take this over, a planet-wide issue, and really be effective.

Mayor Mike Johnston: I think we don’t believe that we should give up here or step away. Our campaign, we call, do more or do less, but do something, whether it’s going to do more in the way of recycling, or less in the way of using a single occupancy vehicle or doing something in terms of being able to make decisions about where and how you use energy. We want to encourage people to take more local action now, in the face of federal abandonment of this. The things that we’ll need help on are the things that made a big difference. The federal tax credits on electrical vehicle purchases — those are big drivers of behavior change. I sponsored when I was in the Senate a state credit that does the same thing — provide incentives, tax incentives for electric vehicle purchases. Here we’re building out aggressively, charging station infrastructure to make it easier for us to convert our fleet vehicles to be electric to get more Ubers and Lyfts and Fedexes and Amazons and UPS (vehicles) to do the same. And to convince regular residents do the same. So we’ll keep building the infrastructure to do this. We’ll keep incentivizing people to do it. We’ll keep changing behavior to do it, and we’ll keep setting our own targets for how our vehicles, our businesses, and our residents try to hit aggressive climate goals, knowing that we’re still all in this together, even if the President doesn’t want to make it a priority.

Anthony Flint: Mike Johnston, Mayor of Denver, Colorado. Thank you once again for this conversation.

Mayor Mike Johnston: Thanks so much for having me, Anthony. It’s great to meet you.

Anthony Flint: You can learn more about all the issues we covered — strategies for affordable housing, sustainable urbanism, transit-oriented development, value capture, and of course, the challenge of climate change, pursuing both mitigation and resilience — all of that and more at the Lincoln Institute website, www.lincolninst.edu. While you’re there, scroll to the bottom and join our mailing list to get periodic updates on our work. And also on social media, the handle is @landpolicy. Finally, don’t forget to rate, share and subscribe to the Land Matters podcast. For now, I’m Anthony Flint, signing off until next time.

Como 39.º alcalde de Providence, Rhode Island, Brett Smiley aborda la seguridad pública, la vivienda asequible, la educación y la resiliencia ante el cambio climático. Antes de ser elegido en 2022, Smiley, quien nació y creció en el área de Chicago y se mudó a Rhode Island para trabajar en política en 2006, fue jefe del Departamento de Administración del estado, director ejecutivo de operaciones de Providence y jefe de personal de la exgobernadora de Rhode Island, Gina Raimondo.

Con una población de alrededor de 191.000 habitantes, Providence es la tercera ciudad más grande en Nueva Inglaterra después de Boston y Worcester, Massachusetts. Esta ciudad, que alguna vez albergó una gran cantidad de fábricas y molinos, en los últimos años se hizo conocida por adoptar el nuevo urbanismo, la preservación histórica y la reutilización adaptativa, así como por sus innovaciones culinarias, culturales y artísticas.

Anthony Flint entrevistó al alcalde Smiley esta primavera en el ayuntamiento. Escuche la conversación completa, que aquí se editó por motivos de longitud y claridad, en el pódcast Land Matters.

La ciudad postindustrial de Providence ha visto crecimiento en población y en ingreso familiar en los últimos años, gracias en parte a una afluencia de residentes con trabajos híbridos o remotos en otras partes. Crédito: Alex Potemkin vía iStock/Getty Images Plus.

Anthony Flint: El arco narrativo de Providence en los últimos 30 años ha sido notable: una ciudad secundaria recuperada del estancamiento económico mediante el desmantelamiento de carreteras, la iluminación de los ríos y el foco en el diseño urbano. Ahora hay preocupaciones sobre la capacidad de pago, comenzando por la vivienda. ¿Hacia dónde se dirige la ciudad ahora?

Brett Smiley: Le agradezco que haya mencionado el notable progreso que ha tenido la ciudad. Hemos recorrido un largo camino, y mientras muchas ciudades postindustriales continúan luchando, Providence está en una trayectoria muy diferente. Gracias a la pandemia, tuvimos una afluencia de personas que comenzaron a reclamar servicios urbanos, arte, cultura, diversidad y transitabilidad a pie, sin que eso conlleve la cantidad de esfuerzo y dinero que implica vivir en Manhattan o Brooklyn, o incluso en Boston.

Uno de los puntos competitivos de la ciudad es que era menos costosa. Pero no pudimos seguir el ritmo desde la construcción y, como resultado, los precios de la vivienda se están disparando. Estamos entre las cinco primeras ciudades en cuanto a afluencia migratoria neta, pero estamos en el puesto 50 de 50 en cuanto a nuevas construcciones de viviendas. Nuestra tarea es facilitar una construcción más densa en el contexto mundial en el que nos encontramos, lo que significa incorporar infraestructura verde para prepararse para el cambio climático y, al mismo tiempo, permitir un mayor crecimiento.

Creemos que podemos liderar el camino para lograr ambos objetivos. Es un momento emocionante para la ciudad. No nos cuesta promocionar Providence. Lo que nos cuesta es asegurarnos de que haya una vivienda disponible para todos los que quieran una.

AF: Hay muchos terrenos vacíos en los que se puede construir, incluidos algunos estacionamientos. Hay lugares que no requieren derribar nada.

BS: Tenemos muchos lugares en donde construir. Uno de nuestros desafíos económicos siempre ha sido que, desde una perspectiva de costos, estamos en el mismo mercado económico que Boston; sin embargo, nuestros alquileres o precios de venta son mucho menores que los de Boston. Tenemos un vacío que llenar en términos del precio que la unidad de vivienda puede exigir y el costo que se necesita para construirla . . . es por eso que estamos trabajando mucho en medidas como incentivos por aumentar la densidad y la flexibilización de los requisitos mínimos de estacionamiento. De esta forma permitimos que los emprendedores inmobiliarios ayuden a que los proyectos sean más viables en cuanto al financiamiento. Además, analizamos algunas soluciones innovadoras que las ciudades de todo el país están probando, como cambios en el código de incendios y otras cuestiones que reducirán el costo de construcción mediante la flexibilización de algunos de los requisitos reglamentarios.

AF: A diferencia de los alcaldes de Boston o París, no ha estado tan entusiasmado con el concepto de calles completas con carriles para peatones, bicicletas y autobuses. ¿Cómo ha evolucionado su forma de pensar?

BS: Sabemos que solo entre el 2 y el 4 por ciento de la población va al trabajo en bicicleta. Aspiramos a duplicar o cuadruplicar ese número. Y, aun así, menos del 10 por ciento de las personas viajarían al trabajo en bicicleta. Queremos que más personas elijan la bicicleta como un medio de transporte alternativo, pero estamos hablando del 5 por ciento de las personas que viajan al trabajo, no del 75 por ciento, aunque a veces se sienta así. Trato de dedicar tiempo y recursos a los medios y métodos de transporte que la mayoría de la gente usa de verdad.

AF: ¿Puede hablar sobre el desafío de retener a los principales empleadores, como el fabricante de juguetes Hasbro, y la práctica de ofrecer beneficios como exenciones fiscales para el desarrollo económico?

BS: Las tácticas para el desarrollo económico han cambiado. El crecimiento significativo que hemos visto en la última década, y en particular desde la pandemia, es que las personas se mudan aquí con buenos trabajos que se encuentran en otro lugar, o directamente en ningún lugar. La forma de pensar en el desarrollo económico ha cambiado, por eso es que la vivienda es una de mis prioridades, porque la vivienda es, de hecho, una estrategia de desarrollo económico.

Sin embargo, los principales empleadores con sede en la ciudad siguen siendo importantes. Las empresas que la gente conoce pueden ser muy relevantes para las perspectivas económicas de la ciudad y su marca, si se quiere. También es valioso asegurarse de que haya una comunidad corporativa central que ayude a apoyar y sostener a las instituciones cívicas, las organizaciones artísticas y otros grupos que dependen del apoyo filantrópico corporativo.

AF: En un estudio reciente, se observó que la vida nocturna de Providence genera casi 1.000 millones de dólares al año en actividad económica, pero se señaló que muchos trabajadores no pueden tomar un autobús para ir a su casa después de que cierran los bares y restaurantes. Ya que carece de un tren o metro ligero, ¿qué puede hacer Providence para mejorar el transporte público?

BS: Es importante que hablemos de la vida durante la noche en general, no solo de la vida nocturna como un entretenimiento. Hay miles de empleados que trabajan durante lo que denominamos “el otro turno de nueve a cinco”: 21:00 a 5:00. Es decir que no solo hablamos de restaurantes, hospitalidad y clubes nocturnos, sino también de las personas que trabajan en el turno noche en un hospital y otros trabajos similares.

No tenemos un sistema de tren o metro ligero aquí en Providence, ni en ningún otro lugar de Rhode Island. Tenemos un sistema de autobuses que funciona bastante bien durante el día, pero es menos frecuente o, en el caso de algunas líneas, deja de funcionar tarde por la noche. Las soluciones son buscar otros medios de transporte, como viajes compartidos y micromovilidad, y que nuestro sistema de autobuses, RIPTA, brinde un mejor servicio a estos grandes centros de empleo. No necesitamos innovaciones de vanguardia. Solo tenemos que pensar en la prestación de servicios para este período que, a menudo, se pasa por alto y se olvida.

Una parada de autobús de la Autoridad del Transporte Público de Rhode Island (RIPTA, por su sigla en inglés) en la Casa del Estado en Providence. Crédito: Christopher Shea/Rhode Island Current.

AF: Dada la experiencia de tener que cerrar un puente importante debido a problemas de integridad estructural, ¿qué piensa sobre la inversión en infraestructura, en particular ahora que las ciudades se podrían enfrentar a un marco diferente del gobierno federal?

BS: Parte de la historia del Puente de Washington en la I-95, que es una arteria importante aquí en la ciudad, es que es un puente de propiedad estatal y un proyecto financiado por el Departamento de Transporte de Rhode Island, que no tuvo el mantenimiento adecuado. La lección que saco de eso es la importancia del mantenimiento continuo para evitar un precio mucho más alto por tener que reemplazarlo. Necesitamos asegurarnos de que todos nos ocupamos de esta infraestructura, en especial después de cuatro años de inversión importante en algunos grandes proyectos de infraestructura aquí en la ciudad y en todo el país. En segundo lugar, necesitamos ingresos predecibles [como las tarifas de los peajes para camiones pesados] para poder pagar estos proyectos. Puedes reparar algo hoy o reemplazarlo mañana, pero el reemplazo siempre es la peor inversión.

AF: Del mismo modo, ¿le preocupa la situación de las instituciones ancla de educación y salud, que siguen siendo un componente clave del renacimiento de Providence, ante las interrupciones en el financiamiento federal?

BS: Estoy muy preocupado por la estabilidad financiera de la educación y la salud. El cambio de la recuperación de costos indirectos para las subvenciones de los Institutos Nacionales de Salud (NIH, por su sigla en inglés) ya está afectando a Providence. Tanto nuestros hospitales como nuestra principal institución de investigación, que es la Universidad de Brown, dependen de esos fondos. Cambiar las reglas a mitad de camino es muy perjudicial.

Los mayores empleadores de la ciudad son el hospital y las facultades. Estos recortes afectarán a nuestra comunidad de una manera u otra, ya sea por la pérdida de empleos, la disminución de los valores inmobiliarios o la menor inversión. Además de todas las oportunidades que podrían no darse como resultado de esto: curas para enfermedades que pueden no descubrirse y soluciones a problemas reales de las que ninguno de nosotros se beneficiaría, si la investigación nunca sucede. Es un problema serio y una verdadera vergüenza. No es forma de tratar a socios importantes.

AF: Usted es un tipo de político diferente en comparación con algunos dirigentes anteriores de Rhode Island que podrían describirse como más de la vieja escuela. ¿Cómo se calificaría en términos de participación con los constituyentes? En una entrevista reciente, dijo: “Hay momentos en que los dirigentes públicos necesitan decir ‘basta, ya hemos escuchado suficiente. Esto es lo que haremos’”.

BS: Suelo abordar los problemas desde dos enfoques: uno relacionado con las prioridades y otro con el estilo. Con respecto a las prioridades, el difunto alcalde de Boston, Tom Menino, a quien no conocí, hablaba de ser un mecánico urbano, [y esa] siempre ha sido una frase con la que me identifico. He tratado de establecer mis prioridades en temas centrales de calidad de vida, cuestiones que afectan la vida cotidiana de las personas, para tratar de mejorarla. Intento solucionar los problemas que en verdad les importan a las personas.

Creo que habrá una gran erosión en la confianza en el gobierno en general. El antídoto para eso es mostrar competencia, eficiencia y eficacia, en particular a nivel local, porque nuestros residentes nos conocen por nuestros nombres. No les avergüenza decirnos lo que creen que no está funcionando. Trato de mantenerme enfocado en esas cuestiones y no en resolver todos los problemas del mundo, sino en resolver los problemas de un vecindario.

En términos de estilo, soy una persona bastante discreta y no tengo altas expectativas, no soy grandilocuente, trato de escuchar a la gente. Estamos muy comprometidos con la comunidad. Tratamos de involucrar a la comunidad de nuevas maneras [como usar Zoom y encuestas en línea]. Pero llega un momento en que el líder debe tomar una decisión y seguir adelante. Para eso me eligieron. Volveré a estar en la boleta el próximo año. Si a los votantes de Providence no les gusta, pueden elegir a otra persona.

Siento que es mi trabajo decir: “De acuerdo, hemos escuchado los comentarios de todos. Hicimos modificaciones donde fue necesario. Podemos estar de acuerdo en no estar de acuerdo en otras cuestiones. Esto es lo que haremos en el futuro y el día de la rendición de cuentas será el día de las elecciones”. Me siento muy cómodo con eso. Creo que eso es lo que se necesita para pasar a la acción.

Eso es lo que creo que nuestros residentes quieren que hagamos: pasar a la acción. La inacción es el enemigo del progreso. Es algo de lo que no quiero ser víctima.

Anthony Flint es miembro sénior del Instituto Lincoln de Políticas de Suelo, conduce el ciclo de pódcast Land Matters y es editor colaborador de Land Lines.

Imagen principal: Alcalde Brett Smiley. Crédito: Ciudad de Providence.

Eventos

Accelerating Community Investment (ACI) Lab Atlanta

Junio 3, 2025 - Junio 5, 2025

Offered in inglés

SHARE

The Lincoln Institute’s Accelerating Community Investment (ACI) initiative is partnering with the City of Atlanta to host an ACI Lab to explore innovative policy and financing solutions for increasing access to starter homes in Atlanta. This forum is aimed at sharing current challenges and initiatives, highlighting emerging models, and engaging participants in collaborative problem-solving to redefine the “starter home” for a post-COVID urban context. The event brings together policymakers, public finance professionals, urban developers, community organizations, and impact investors engaged in affordable housing locally in Atlanta and nationally through the ACI community of practice.

This event is by invitation only.

Detalles

Fecha(s)

Junio 3, 2025 - Junio 5, 2025

Idioma

inglés

Palabras clave

desarrollo económico

The Lincoln Vibrant Communities Fellows Program, May 2026

The Lincoln Vibrant Communities Fellows Program is a 24-week program designed to build capacity to address challenges in communities using the best practices, tools, and research of the Lincoln Institute of Land Policy and the academic excellence of Claremont Lincoln University. This collaborative program offers graduate-level education, expert connection, and peer networking to support public and private sector leaders in advancing sustainable community development.

Participants will engage in immersive in-person education; an online leadership curriculum; and specialized coursework covering concepts such as scenario planning, data visualization, strategic communication, conflict mediation, and policy development. The program culminates in a nine-credit graduate certificate in Advanced Public Sector Leadership, providing a pathway for further academic and professional growth.

Through applied learning, expert-led discussions, and collaboration, fellows will develop innovative solutions to enhance resilience and inspire impactful change. Graduates join a national network of leaders dedicated to fostering sustainable, engaged communities. Fellows are highly encouraged to consider participating in the Teams Program following completion of the Fellows Program.

The online application form will open on March 17, 2026. Applications are due by April 22, 2026. The program begins on May 13, 2026, in Chicago, IL. A limited number of early applicants will receive a Claremont Lincoln University sweatshirt to celebrate joining the next cohort of leaders.

This program, which is partially underwritten, costs $2,500 per participant. Please see the application guidelines for further details.

Detalles

Registration Deadline

April 22, 2026 at 11:59 PM

Palabras clave

desarrollo económico, gobierno local, planificación

Providence, Rhode Island is a unique story—a “second city” in the orbit of significantly larger Boston to the north, but punching above its weight as a desirable place to live and work. With a population of nearly 200,000 people, it’s the third largest city in New England after Boston and Worcester, Massachusetts, and was once home to extensive manufacturing and mills—a classic smaller legacy city, making its way in a postindustrial world.

Key city-building strategies have driven revitalization over the last 30-plus years. Providence became known for embracing New Urbanism, historic preservation, and adaptive reuse in its traditional downtown, and for culinary, cultural, and arts innovations like WaterFire, a festival of lanterns along three downtown rivers. The Congress for the New Urbanism is returning to Providence in June of this year for its annual summit.

At this juncture in the remarkable narrative, after dismantling highways and daylighting rivers and paying attention to urban design, the Renaissance City is now grappling with concerns about affordability, failing schools, crumbling infrastructure, and lingering pockets of post-manufacturing blight

All of that is the scenario for Brett P. Smiley—once chief of staff for former Rhode Island Governor Gina Raimondo—who was elected the 39th mayor of Providence in 2022. In this latest episode of the Land Matters podcast, and as part of the continuing series Mayor’s Desk—interviews with local leaders tackling global problems—Smiley talks about the challenges of keeping up the city’s revitalization momentum while addressing stubborn disparities.

“We’ve come a long way, and while there’s many of these kinds of postindustrial cities that continue to struggle, Providence is on an entirely different trajectory,” Smiley says. “Through the pandemic, a lot of people moved to Providence—primarily from the major population centers of New York and Boston, but from really around the country—where you saw people still wanting urban amenities, still wanting arts and culture and diversity, walkability, but with a little bit less work than it is to live in Manhattan or Brooklyn, certainly less expensive than living in those places or in Boston.”

While welcoming the influx, he says, “We’ve not kept pace with building, and as a result, housing prices are skyrocketing. That was in fact one of our competitive points in that we were less expensive. In the decade ahead, we’ve got a lot of work to do to bring down the cost of housing. What we have is a supply shortage and the solution to that is to build more.”

Also in the interview, Smiley reflects on his contrarian views on bike lanes, how to better support night-shift workers with improved transit and other services, housing as an economic development strategy to attract and retain major employers, and his experiences engaging with constituents.

He also shares his thoughts on how to balance public input with policy leadership; he was quoted earlier this year as saying, “There are times when public leaders need to say, ‘Pencils down, we’ve heard enough. This is what we’re doing.’”

Smiley came into office promising to prioritize public safety, education, affordable housing, and climate resilience, relying on “strategic investments and data-driven solutions.” Before being elected mayor, he was head of the Rhode Island Department of Administration and chief operating officer of Providence. Smiley graduated from DePaul University with a degree in finance and an MBA. He resides on the East Side with his husband, Jim DeRentis, their dog, and their two cats.

En el barrio de Carondelet en St. Louis, donde los astilleros que alguna vez estuvieron ocupados dieron paso a espacios vacíos y abandonados durante las últimas décadas del siglo XX, una compañía global de minerales especializados está construyendo una fábrica de US$ 400 millones para producir baterías de alta eficiencia para el almacenamiento de energía.

Recientemente, se levantó una nueva fábrica en medio de las acerías y las minas de carbón cerradas de Weirton, Virginia Occidental, construida por un fabricante diferente cuya tecnología de baterías consiste en mezclar partículas de hierro y aire.

Y en Schenectady, Nueva York, donde la producción de luces, electrodomésticos y motores eléctricos por parte de la compañía General Electric (GE) de Thomas Edison estimuló un auge económico que comenzó a fines del siglo XIX y se había desvanecido a mediados del siglo XX, la primera de una clase de turbinas eólicas terrestres súper altas y de alta eficiencia recientemente salió de una línea de ensamblaje prístina en una nueva planta de GE.

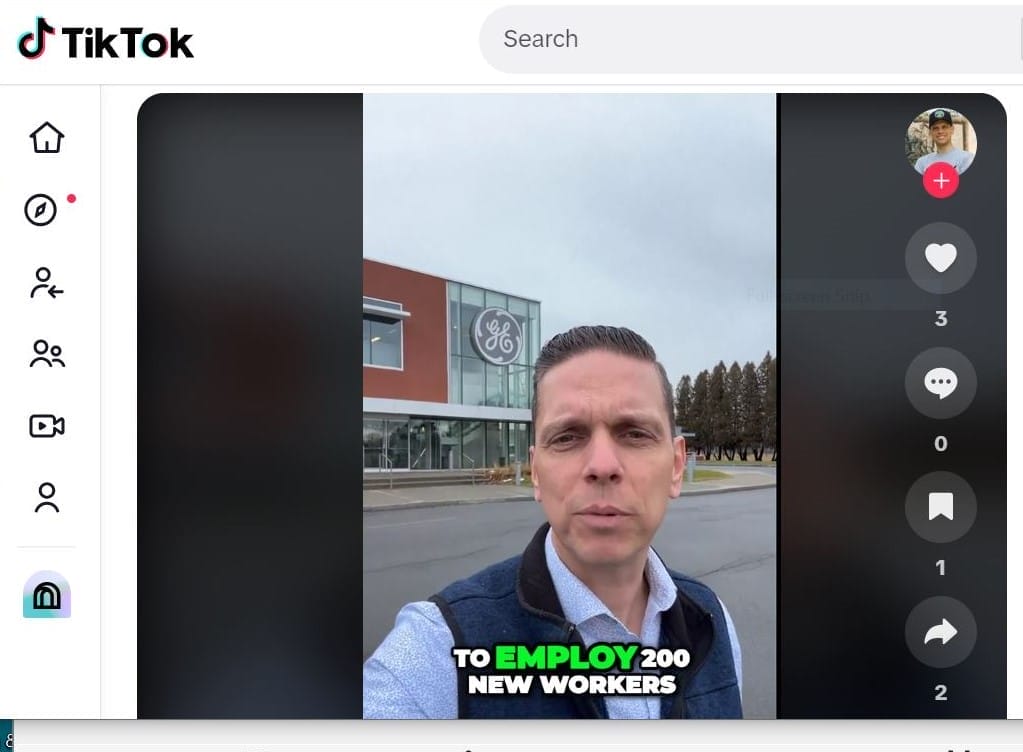

“Es un beneficio mutuo para el medio ambiente y la fuerza de trabajo local”, dijo el asambleísta del estado de Nueva York, Angelo Santabarbara, en un video de TikTok grabado fuera de la planta, que llegará a emplear a 200 personas, incluida la mano de obra calificada del sindicato. El resultado final, dijo, será “un futuro energético más asequible, confiable, sostenible y seguro”.

El legislador neoyorquino, Angelo Santabarbara, elogia el auge de la energía limpia en TikTok. Crédito: Oficina del legislador Santabarbara.

Todos estos proyectos y docenas más en todo el país son manifestaciones de una nueva política industrial federal basada en el lugar, impulsada por más de US$1 billón en créditos fiscales y subvenciones en virtud de la Ley de Empleo e Inversión en Infraestructura, el Plan de Rescate Estadounidense, la Ley de CHIPS y Ciencia, y sobre todo, lo que en esencia es una legislación de acción climática radical, la Ley de Reducción de la Inflación.

Ante la necesidad urgente de fabricar los componentes de la transición a energía limpia (vehículos eléctricos, baterías y almacenamiento de energía, equipos para estaciones de carga, turbinas eólicas, paneles solares y muchas otras piezas de la transición sin combustibles fósiles, como líneas eléctricas de fibra de carbono de alta capacidad para reforzar la red eléctrica sobrecargada del país), la administración de Biden ha tomado varias decisiones estratégicas.

En primer lugar, la Casa Blanca declaró que los Estados Unidos no debería ceder toda esta industria avanzada a China, que es el actual líder mundial en la producción de equipos eólicos y solares y vehículos eléctricos baratos. Y si estos artículos se van a fabricar en los Estados Unidos, según dicen los funcionarios de la administración, debería suceder en antiguas ciudades industriales y condados empobrecidos: los “lugares donde la oportunidad se ha ido”, como dijo el asesor climático de la Casa Blanca, Ali Zaidi, en una conferencia de la Universidad de Columbia el otoño pasado.

Desde que el presidente Biden asumió el cargo, las empresas han anunciado más de US$250.000 millones en inversiones privadas, una cantidad sin precedentes, para fabricar “las tuercas y los tornillos de la energía limpia”, dijo Ben Beachy, asistente especial del presidente para Política Climática, Sector Industrial e Inversión Comunitaria. “La administración se compromete a garantizar que las comunidades y los trabajadores más afectados cosechen las recompensas de este auge, incluidas las comunidades desindustrializadas”, dijo Beachy.

Los dirigentes de las antiguas ciudades industriales, que han estado luchando con la pérdida de producción y población durante décadas, dicen que reciben el impulso con gratitud. Muchos perciben algo poético sobre el reemplazo de procesos de fabricación altamente contaminantes de hace un siglo por una industria que funciona de manera sostenible y que produce equipos que ayudarán a reducir las emisiones de combustibles fósiles. El pivote, tanto cultural como en relación con el desarrollo económico, ya está llevando a algunos a llamar el Medio Oeste y el Sureste el “cinturón de baterías”.

“Ciudades como la nuestra han crecido en base a la innovación energética, pero eso tuvo un precio”, dijo Paige Cognetti, alcaldesa de Scranton, Pensilvania, una ciudad conocida desde principios del siglo XX por sus industrias de carbón y electricidad que generaban hollín. Cognetti cita las raíces de Biden en la ciudad de clase obrera como factor en la iniciativa para ayudar a las antiguas ciudades industriales a participar en la transición a la energía limpia: “Creo que entiende que son necesarias grandes inversiones para preparar regiones para el éxito económico y la resiliencia ante el cambio climático”.

Sin embargo, quedan muchas preguntas sobre la implementación, entre ellas, si las regiones económicamente empobrecidas pueden hacer aparecer, por arte de magia, el ecosistema necesario para apoyar a la nueva industria: primero que todo, una fuerza laboral capacitada, pero también otros elementos como infraestructura, viviendas e instituciones cívicas y de educación superior activas para proporcionar no solo capacitación sino también investigación y desarrollo.

Además, la enorme cantidad de inversión federal que fluye de Washington requerirá una gran capacidad administrativa a nivel estatal y local para descubrir las oportunidades, gestionar las transacciones, y cumplir con las normas y regulaciones.

Por último, se espera que los problemas de uso del suelo compliquen el esfuerzo. La cantidad de espacio que necesitan muchas de las empresas privadas, en particular, para construir vehículos eléctricos, es tal que los mejores sitios se encuentran en la periferia de las ciudades que requiere un desarrollo totalmente nuevo, en lugar de en el núcleo urbano. El redesarrollo en terrenos urbanos vacíos es posible, pero la reutilización adaptativa y la regeneración de terrenos abandonados implica un importante aumento de los costos.

Los desafíos son muy reales, pero también lo es la oportunidad. Si bien el gasto federal de la IRA podría verse interrumpido con un cambio en las administraciones, la derogación requeriría una acción del Congreso. Mientras tanto, miles de millones de dólares en fondos federales han comenzado a fluir de las primeras inversiones de esa ley. Los gobiernos locales, regionales y estatales y sus socios deben estar listos con planes reflexivos y viables para su implementación, dijo Peter Colohan, director de Estrategias Federales del Instituto Lincoln de Políticas de Suelo.

“El dinero y los incentivos que salen del gobierno a un ritmo acelerado están haciendo que la inversión privada sea irresistible: en energía limpia, soluciones climáticas basadas en la naturaleza y fabricación avanzada”, dijo. Añadió que los problemas del uso del suelo y la equidad surgirán con regularidad, lo que demandará que los gobiernos estatales y locales, las organizaciones filantrópicas y las organizaciones sin fines de lucro ayuden a “crear círculos virtuosos de inversión comunitaria y evitar daños no deseados”.

* * *

La historia de los subsidios en la manufactura estadounidense tiene algunas complicaciones, pero en última instancia, el gobierno ha apoyado a la industria de una forma u otra durante más de dos siglos. Desde los primeros molinos de harina a fines del siglo XVIII hasta el advenimiento de la línea de ensamblaje automotriz, la fabricación en los Estados Unidos satisfizo una necesidad del mercado de bienes y suministros que fue impulsada en gran medida por el espíritu empresarial individual, aunque en general fue recibida con los brazos abiertos por funcionarios locales felices de asegurarse de que las transacciones de tierras, por ejemplo, se realizarán sin problemas para establecer fábricas y viviendas de trabajadores cercanas.

Durante esa primera era de crecimiento industrial, el gobierno también intervino para proporcionar la infraestructura necesaria para apoyar el comercio, desde una red ferroviaria nacional hasta puertos y canales. Las fábricas solían ubicarse bien cerca de los límites de la ciudad, ya que su acceso a las vías fluviales y las líneas ferroviarias hacía que fuera bastante fácil llevar los productos al mercado, tanto el nacional como el extranjero. La huella física de este crecimiento en las ciudades de los Estados Unidos fue transformadora, con estructuras de muchos pisos que se extendían por varias cuadras construidas para emplear a 10.000 trabajadores o más, y una densidad adyacente de viviendas y servicios.

Las principales fábricas y sucursales de Westinghouse Electric & Manufacturing Company en Pittsburgh, alrededor de 1905. Crédito: Biblioteca del Congreso.

La Segunda Guerra Mundial orientó el poderío industrial de la nación hacia la construcción de tanques y aviones para los militares, y comenzó una tradición de gastos en defensa descentralizados, con contratistas que se establecieron en los distritos del Congreso que se aseguraron de que los fondos del Pentágono siguieran fluyendo. La Ley de Carreteras Interestatales de 1959 fue otra importante fuente de inversión federal para las ciudades, impulsada por el argumento de que se necesitaba una infraestructura de autopistas nueva para el rápido movimiento de mercancías.

Cuando las economías de Japón y Europa se reactivaron en las décadas posteriores a la guerra, la fabricación en las ciudades del Cinturón del Óxido fue disminuyendo de forma gradual. Desde la década de 1950 hasta la década de 1970, las empresas privadas fueron aprovechando cada vez más la mano de obra más barata del extranjero, y la automatización tecnológica en la producción y la distribución redujo aún más la nómina. Así comenzó el declive de las ciudades que supieron ser prósperas en una franja que abarcaba desde el río Mississippi hasta el noreste, desde St. Louis hasta Cleveland, Allentown hasta Hartford.

La avalancha de cierres de fábricas durante la década de 1970 fue devastadora, dijo Alan Mallach, coautor de Regenerating America’s Legacy Cities (La regeneración de las antiguas ciudades industriales de los Estados Unidos), un informe de enfoque político publicado por el Instituto Lincoln. “Comience con la propuesta de que, en la década de 1950 y principios de la década de 1960, la mitad de todos los empleos en ciudades como Cleveland o Youngstown se concentraban en la manufactura, y luego tenga en cuenta que la mayoría de los empleos minoristas y de servicios tenían el soporte de salarios que ganaban los trabajadores de las fábricas, hay que calcular que del 70 al 80 por ciento de las economías locales en estas ciudades se basaban en su sector de manufactura. Así que ‘condenado’ puede ser un poco fuerte, pero se acerca”.

Agregue el fenómeno de la fuga blanca en el que los residentes blancos se movían en masa desde las áreas urbanas del centro hasta los suburbios, y lo que es notable es que las antiguas ciudades industriales sobrevivieron de cualquier modo, dijo Mallach. Dice que, con un entorno urbano físico y un tejido social y económico que atravesaba un cambio drástico, “gran parte del crédito se atribuye a las miles de familias negras de clase obrera y clase media que se mudaron a los barrios desocupados por familias blancas y los estabilizaron durante las próximas décadas”.

Durante el último medio siglo, ciertos tipos de manufactura continuaron siendo apoyados ad hoc por el gobierno de los Estados Unidos, en forma de aranceles selectivos, impuestos a competidores extranjeros para beneficiar al acero fabricado en los Estados Unidos, por ejemplo, o rescates directos, como los que gozó la industria automotriz después de la Gran Recesión. Mientras tanto, las empresas de tecnología, incluida Amazon, han recibido con frecuencia un tratamiento de alfombra roja que implica importantes exenciones fiscales y otros incentivos, dado que los dirigentes locales compiten para que las empresas se establezcan en su ciudad o pueblo.

En particular, es el sector energético el que se ha beneficiado de la historia de subsidios más larga y sólida, desde los incentivos federales por el agotamiento de los pozos de petróleo en la década de 1920 hasta las exenciones fiscales y los subsidios hasta el día de hoy, que se estiman, en base a un cálculo prudente, en US$20.000 millones al año para productores de carbón, gas natural y petróleo crudo.

Ahora que los combustibles fósiles están listos para el reemplazo por energías renovables, incluidas la eólica, la solar y la hidroeléctrica, la Casa Blanca está tratando de ejecutar el equivalente a una jugada de billar a tres bandas: combatir el cambio climático impulsando una transición sin combustibles fósiles, fabricar componentes y sistemas de energía limpia en los Estados Unidos y restaurar empleos en lugares con dificultades.

“No lograremos nuestros objetivos climáticos sin movilizar billones de dólares en apoyo de la acción climática. Con una guía adecuada, esa ola de inversiones puede fluir hacia buenos empleos sindicalizados”, dijo Beachy, de la oficina federal de Política Climática. “Con una guía adecuada, puede fluir hacia las comunidades que han soportado décadas de desinversión. Nuestra estrategia climática es una estrategia de trabajo, es una estrategia de equidad. Esa es la lógica básica”.

Para una iniciativa que ha estado operando relativamente bajo el radar, el enfoque basado en el lugar parece haber tenido un buen comienzo. Según dos bases de datos del gobierno federal, en el Departamento de Energía y el inventario Invirtiendo en Estados Unidos de la Casa Blanca, se estima que 700 proyectos de energía limpia ya están en curso o en proceso, en sectores que incluyen los siguientes:

Baterías y materiales: las baterías de alto rendimiento son muy demandadas por los vehículos eléctricos cada vez más populares, incluido el Ford F150. El almacenamiento de energía es una gran necesidad en la red de energía limpia para extender y preservar la energía proporcionada por las energías renovables. Impulsadas por la innovación, las fábricas de baterías y las instalaciones de minerales críticos están surgiendo en Michigan (Our Next Energy), Georgia (Anovion Tech, SK Battery), Carolina del Norte (Albemarle Corp.) y Mississippi, donde una nueva iniciativa conjunta de baterías de camiones creará más de 2.000 empleos, más que cualquier inversión individual que se haya realizado en el estado.

Vehículos eléctricos: dada la ventaja de los fabricantes de vehículos eléctricos con sólidos subsidios en China, así como la posición competitiva de la empresa pionera Tesla, la expansión de la producción en los Estados Unidos se ha detenido. Los funcionarios de la administración dicen que hay una creciente demanda, ayudados por el crédito fiscal de US$7.500 que las personas pueden reclamar al momento de la compra; desde la aprobación de la IRA en 2022, hubo un récord de 1,46 millones de ventas de vehículos limpios para pasajeros, según el Departamento del Tesoro. Además de las nuevas plantas de vehículos eléctricos, como la de Rivian en Illinois, hay miles de millones disponibles para remodelar las instalaciones de fabricación de automóviles existentes y fomentar la fabricación y el despliegue de la importante red de estaciones de carga, cuya presencia está a punto de ser tan generalizada como la de las estaciones de servicio.

Viento: una vez más, China es el principal productor de turbinas eólicas, con el 60 por ciento de la capacidad de producción mundial. Pero las empresas estadounidenses, como GE Vernova en Schenectady, están avanzando en el desarrollo de torres, aspas e infraestructura asociada más eficaces y eficientes para mejorar la conectividad a la red. Las innovaciones tecnológicas también están abriendo nuevas posibilidades, como turbinas sin aspas menos costosas que capturan los vientos dominantes o giran para capturar el viento desde diferentes direcciones.

Solar: la fuente de energía de más rápido crecimiento del mundo es otro desafío complejo, ya que los paneles solares más baratos continúan fabricándose en China y, de hecho, las siete principales compañías solares chinas proporcionaron recientemente más energía al mundo que las compañías petroleras, según Bloomberg. Pero algunos destacados han tenido éxito, en particular, es poético en lugares que solían producir carbón o manufacturas pesadas. En Farmington, Nuevo México, se está construyendo una granja solar cerca de una planta de energía a carbón y una mina desmanteladas. Al igual que con la tecnología eólica, la energía solar está evolucionando con rapidez; una empresa ha desarrollado esferas de cristal que captan el sol y que ocuparían una fracción del espacio que ahora se requiere para los paneles.

Otros apoyos auxiliares: varios programas bajo la IRA están brindando apoyo general a la nueva industria mediante la mejora de carreteras, puentes, aeropuertos y sistemas de agua potable, con mejoras notables en las obras en Milwaukee, Buffalo y Allentown. La Casa Blanca también tiene la intención de reforzar la cadena de suministro de materiales como el aluminio, que es fundamental en los paneles solares, los vehículos eléctricos y las líneas eléctricas, y asegurarse de que la producción de esos materiales sea menos contaminante. Por ejemplo, Century Aluminum está recibiendo fondos del Departamento de Energía para un proyecto de US$3.900 millones para construir una nueva planta de fundición de aluminio primario limpia en la cuenca del río Mississippi.

Este generador aerodinámico sin aspas, desarrollado por Aeromine, está diseñado para su uso en tejados grandes y planos. Crédito: Aeromine.

Es difícil exagerar el volumen sin precedentes de apoyo federal para estos esfuerzos. Hacer un seguimiento de los fondos disponibles y hacia dónde se dirigen se ha convertido en una industria artesanal. En parte porque el principal instrumento es el crédito fiscal, el costo final para el presupuesto federal depende de la cantidad de empresas privadas que colaboran con las regiones locales en los proyectos (así como de los hogares individuales que aprovechan los descuentos para los vehículos eléctricos, la eficiencia energética y los sistemas respetuosos con el clima, como las bombas de calor para climas cálidos y fríos).

La cifra de referencia compartida por la administración Biden fue que la IRA, un programa plurianual, proporcionaría al menos US$370.000 millones para la transición hacia la energía limpia, en gastos y créditos fiscales. La Brookings Institution estima que US$780.000 millones podrían estar circulando por la economía estadounidense para 2031, mientras que Goldman Sachs calcula el monto potencial total en US$1,2 billones.

“Es un momento político extraordinario”, dijo Mark Muro, miembro sénior de Brookings, quien fue coautor de un informe que enumera unos 70 condados en dificultades que ya han recibido algún tipo de inversión. “Esta es una estrategia industrial nueva, moderna y claramente estadounidense, que reequilibra la economía. Esto traerá esperanza y actividad económica genuina a lugares que no han tenido eso durante años”.

Los partidarios señalan docenas de inauguraciones de plantas que ya han ocurrido, parte de lo que comparan con los fabricantes que se presentaron para el esfuerzo de guerra hace más de 80 años, como una especie de movilización nacional patriótica simbolizada por Rosie, la remachadora, que flexiona el bíceps y proclama: “Podemos hacerlo”.

De dónde proviene el financiamiento

En teoría, la administración de Biden ha puesto a disposición más de US$3,6 billones en fondos federales para infraestructura, fabricación y resiliencia comunitaria desde 2021, incluidos cientos de miles de millones para apoyar la transición sin combustibles fósiles (Carey y Shepard 2022). En la actualidad, solo se ha distribuido una fracción del compromiso de gasto plurianual.

Ley de Reducción de la Inflación (IRA, por su sigla en inglés): La característica principal de esta ley de casi US$500.000 millones firmada por el presidente Biden en 2022, además de las medidas para frenar la inflación, como la reducción del déficit presupuestario federal y la reducción de los precios de los medicamentos recetados, es una inversión sin precedentes en energía limpia para combatir el cambio climático. La IRA, un plan de gastos plurianual basado en gran medida en créditos fiscales, podría tener un costo total de US$1 billón, según algunas estimaciones.

Ley de CHIPS y Ciencia (CHIPS): También promulgada en 2022, la Ley de Creación de Incentivos Útiles para Producir Semiconductores (CHIPS, por su sigla en inglés) y Ciencia tiene la intención de volver a fabricar microchips en los Estados Unidos después de décadas de fabricación de semiconductores en el extranjero, en su mayoría, en China. Se están destinando alrededor de US$60.000 millones para fortalecer la fabricación estadounidense, las cadenas de suministro y la seguridad nacional, e invertir en investigación y desarrollo para la industria de alta tecnología, incluida la nanotecnología, la energía limpia, la computación cuántica y la inteligencia artificial.

Ley de Empleo e Inversión en Infraestructura (IIJA, por su sigla en inglés, también conocida como la Ley de Infraestructura Bipartidista): Esta ley autoriza US$1,2 billones en gastos que incluyen alrededor de US$550.000 millones en fondos para carreteras y puentes de los Estados Unidos, infraestructura de agua, Internet y más. La Casa Blanca describe la legislación, promulgada en 2021, como un impulso a la competitividad de los Estados Unidos que creará empleos y “hará que nuestra economía sea más sostenible, resiliente y justa”.

Ley del Plan de Rescate Estadounidense (ARPA, por su sigla en inglés): Este paquete de estímulo nacional de US$1,9 billones, aprobado por el Congreso y firmado por el presidente Biden, incluyó US$30.500 millones en fondos federales para apoyar los sistemas de transporte público de la nación y otras inversiones de capital. La legislación, promulgada en 2021, fue en gran medida una respuesta a la perturbación económica causada por la pandemia de la COVID.

* * *

Aunque la generosidad federal es bienvenida, algunos se preguntan si una sola fábrica en verdad puede lograr reducir los problemas de la pobreza profundamente arraigada, las escuelas de bajo rendimiento, las propiedades vacantes y el crimen persistente que han hecho metástasis durante décadas en las antiguas ciudades industriales.

“La reindustrialización en torno a la energía limpia y la tecnología es algo bueno hasta donde llega, pero no creo que vaya tan lejos como sus impulsores parecen creer”, dijo Mallach. Hay una gran carga que superar. El renacimiento en lugares como Cleveland o St. Louis ha sido desigual. Algunas antiguas ciudades industriales más pequeñas han tenido problemas en parte debido a la falta de instituciones cívicas sólidas e instituciones de educación y salud, las instituciones ancla sin fines de lucro que brindan empleo e innovación.

La ciudad industrial tradicional se sustentaba en una especie de fábrica que ya casi no existe: instalaciones con grandes huellas y que emplean a 10.000 personas o más. Esa configuración no se reemplaza con facilidad, dijo Mallach. La nueva fabricación requiere mucha menos mano de obra.

Como ejemplo, citó una nueva fábrica de acero en Youngstown, Vallourec Star, que reemplazó una instalación anterior. “Puede que produzca más que el antiguo molino, pero lo hace con 700 a 800 trabajadores, no con 10.000 a 15.000. Y la mayoría de esos trabajadores se sientan frente a consolas y operan maquinaria y robots, lo que, por supuesto, significa que necesitan un nivel significativo de conocimiento informático. Ahora, 700 puestos de trabajo son importantes, pero es una gota en el mar en comparación con lo que se ha perdido”, dijo Mallach.

Otros tienen preocupaciones a un nivel político más alto, ya que expresan dudas sobre la capacidad del gobierno para elegir ganadores y perdedores en los mercados privados, y recuerdan el fracaso de la empresa de energía solar Solyndra durante la administración de Obama. Algunas empresas emergentes no funcionan. Es posible que los mineros del carbón no puedan pasar a ser electricistas en una fábrica de turbinas eólicas. El fabricante de vehículos eléctricos, Rivian, ya tuvo que detener la construcción de una planta de 1 millón de metros cuadrados en Georgia debido a pérdidas financieras a la vez que la compañía intenta aumentar la producción.

“Creo que debería haber un criterio bastante exigente para justificar” el apoyo del gobierno a la industria privada, dijo Colin Grabow, director asociado del Cato Institute. “Si hay alguna necesidad que el mercado no está satisfaciendo, el gobierno podría intervenir”, dijo, o si hay problemas de seguridad nacional en juego, como es el caso de los microprocesadores.

Pero Grabow también cuestiona la política industrial emergente en términos prácticos, y plantea que el mundo debería tener acceso a la energía limpia más barata posible, ya sea hecha en los Estados Unidos o no.

“Si el objetivo primordial dice: ‘oye, nos enfrentamos a una emergencia planetaria y tenemos que hacer esta transición’, . . . si los chinos quieren darnos vehículos eléctricos y celdas solares baratos y todo lo demás, entonces eso debería ser bienvenido. La economía y el empleo deberían pasar a un segundo plano”, dijo. Aun así, los partidarios argumentan que, si alguna vez hubo un momento para impulsar la transición hacia la energía limpia, es ahora, ya que básicamente el futuro del planeta está en juego. Muchos lamentan un patrón que se percibe en el que el sector de la energía limpia se está examinando y cuestionando sin razón, a la luz de la historia del gobierno de apoyar con tanto empeño a otras industrias.

Dirigir las fábricas hacia regiones postindustriales se considera una medida apropiada para abordar las desigualdades económicas, en especial en aquellos lugares que, a fin de cuentas, se vieron perjudicados por los impactos medioambientales y de salud de la minería del carbón u otras industrias altamente contaminantes.

“Lidiar con el cambio climático también ofrece una oportunidad real de enfrentar la desigualdad que afecta a nuestro país”, dijo Bill McKibben, profesor de Middlebury College y fundador de las organizaciones de acción climática 350.org y Third Act. La administración Biden “ha estado colocando fábricas en lugares en base a necesidades reales”.

Hasta ahora, los fondos federales para apoyar la fabricación de energía limpia hecha en los Estados Unidos se destinan a los estados azules y rojos por igual y, de hecho, un análisis de Politico mostró que la mayoría de los proyectos se encuentran en estados rojos.

“Queremos ser capaces de producir energía limpia en todos los rincones del país. Estados azules, estados rojos, en realidad ayuda a ahorrar dinero a la gente, así que todo se trata de lo verde”, dijo la secretaria de Energía de los Estados Unidos, Jennifer Granholm, a los periodistas en una sesión informativa de la Casa Blanca el año pasado cuando explicó cómo los distritos republicanos estaban utilizando las inversiones en energía limpia.

La secretaria de Energía, Jennifer Granholm, en el centro, con el gobernador de Misuri, Mike Parson, y otros funcionarios en la inauguración de 2023 de la planta de fabricación de materiales de baterías de ICL en San Luis. Crédito: ICL.

Sin embargo, quedan al menos tres desafíos principales para que la implementación de la política industrial basada en el lugar tenga éxito. El primero es la capacidad de los gobiernos estatales y locales para aprovechar todos los fondos y programas que se han puesto a disposición con mucha rapidez.

Los estados y municipios están luchando para postularse para docenas de nuevos programas a fin de aprovechar los créditos y reembolsos fiscales, lo que requiere un amplio conocimiento de las reglas de otorgamiento de subvenciones y cumplimiento. La administración ha tratado de hacer que el proceso sea lo más fácil posible para el usuario y ha establecido el “pago directo”, que extiende la elegibilidad para recibir fondos a organizaciones sin fines de lucro y municipios, por primera vez. “Si calificas, obtienes un cheque”, dijo el asesor sénior de la Casa Blanca, John Podesta, a los funcionarios estatales y locales en la reunión de invierno de la Conferencia de Alcaldes de los EE. UU. en enero en Washington D. C. “Esperamos que sean evangelistas” en la difusión de la palabra, agregó.

A pesar del esfuerzo, seis de cada diez alcaldes dijeron en una encuesta realizada por la Initiative on Cities (Iniciativa de Ciudades) de la Universidad de Boston que las complejidades burocráticas estaban entorpeciendo el proceso, e hicieron referencia a un “desafiante proceso de solicitud de subvenciones y la falta de familiaridad del público con sus detalles”.

Algunos estados como Illinois y Nevada han establecido oficinas para asegurarse de que los fondos federales se utilicen de manera eficiente y efectiva. Recientemente, Massachusetts también hizo algo similar, para ayudar a informar a las comunidades en dificultades sobre las oportunidades de financiamiento federal que pueden ayudar a fomentar el interés de la inversión privada. Randall Woodfin, el alcalde de Birmingham, Alabama, estableció un “centro de mando” para realizar un seguimiento de las solicitudes y los plazos.

Otro obstáculo más complicado es la necesidad de apoyar las fábricas nuevas con un ecosistema que incluya la capacitación de la fuerza laboral, el cuidado de niños y el importante compromiso de las instituciones sin fines de lucro, cívicas y de educación superior. Y eso, a su vez, guiará las decisiones de uso del suelo que desbloquearán la actividad económica de manera equitativa, dijo Bruce J. Katz, director del Nowak Metro Finance Lab (Laboratorio de Finanzas Metropolitanas de Nowak) en la Universidad Drexel.

“Es una transición notable. Es extraordinaria. Pero la ubicación es importante”, dijo Katz, quien también es cofundador de New Localism Advisors, que busca ayudar a las ciudades a diseñar, financiar y ofrecer iniciativas transformadoras que promuevan el crecimiento inclusivo y sostenible. “El diablo está en los detalles cuando se trata del lugar donde se encuentran las grandes plantas, y todas estas piezas del rompecabezas deben unirse, ya sea la cadena de suministro, los efectos secundarios, o la preparación de la fuerza de trabajo”.

El país “tiende a tener una perspectiva del mundo en la que se invierte primero y se planifica después”, dijo, lo que lleva a un sistema con un alto nivel de descentralización. “Abrimos el grifo y la inversión corporativa está allí lista. Bueno, las ciudades deben tener los sitios listos”.

Además de determinar las ubicaciones adecuadas, agrega Amy Cotter, directora de Sostenibilidad Urbana en el Instituto Lincoln, “las ciudades van a necesitar tener una intención concreta sobre la planificación de una industria nueva en coordinación con la resiliencia y la inclusión”. El planeamiento urbano reflexivo, señala, “puede dar lugar a una industria limpia en un ecosistema de apoyo que mejore la prosperidad equitativa tanto para los residentes antiguos como para los nuevos”.