The Unintended Consequences of Assessment Limits

Click on the links in the introduction below to read about each topic in more detail.

Assessments limits are a common policy tool to lessen the impact of rising property values on tax assessments in the belief that this will lead to lower tax bills. These limits, however, are among the worst options for property tax relief. They can lead to significant inequity:

- Taxpayers can pay many times more than owners of property with the same value, and at a higher rate than more valuable properties.

- Long-term owners benefit at the expense of owners who purchased their property more recently.

- Rapidly appreciating property, often in more affluent areas, is subsidized by properties whose values are stagnant or even declining.

- Even taxpayers whose assessed value is limited by the cap may pay more than they would if there were no limit on assessment growth.

All these factors create distortions that reduce local economic competitiveness.

Once assessment caps are implemented, they can be nearly impossible to repeal if taxpayers whose property values have grown the most would see sharp, immediate tax increases. This makes it even more important to avoid assessment limits in the first place.

There are better ways to provide Property Tax Relief for Homeowners when values rise, including circuit breakers, homestead exemptions, tax deferrals, and monthly payment options. If controlling increases in overall property tax revenue is a concern, Truth in Taxation programs can effectively prevent “silent” increases in tax bills when values rise but tax rates are kept level.

What is an assessment limit?

Assessment limits set a cap on annual increases in the assessed value of individual properties, regardless of changes in market value. They are intended to protect homeowners from property tax increases when real estate values rise rapidly.

Why are limits on the growth of assessments popular?

Taxpayers value predictability in their property tax payments, with taxes remaining level or growing near the pace of their incomes. However, real estate markets can be volatile and unpredictable. Senior taxpayers living on a fixed income are particularly vulnerable to spikes in their property tax payments that result from rising home values.

These problems can be compounded when jurisdictions do not regularly update their assessments to market levels. If revaluation cycles are long, or if courts and legislatures require a long-delayed revaluation, several years of accumulated market increases can create sudden spikes in assessments.

In these situations, policymakers are often tempted to restrict or limit increases in assessments, believing that will limit property tax increases and meet the taxpayer’s desire for predictability.

However, this predictability reduces equity in the tax system, often significantly. Assessment limits can also cause many taxpayers to owe more in property taxes than they would if there were no limit.

Assessment limits create large disparities in tax bills for owners of similar homes.

Equity in property taxes usually refers to the fairness and uniformity with which properties are assessed and taxed. An equitable tax system ensures that properties with similar market values pay similar taxes.

Assessment limits prevent property taxes from responding to changes in market value. As a result, it is impossible for assessments and tax bills to remain equitable.

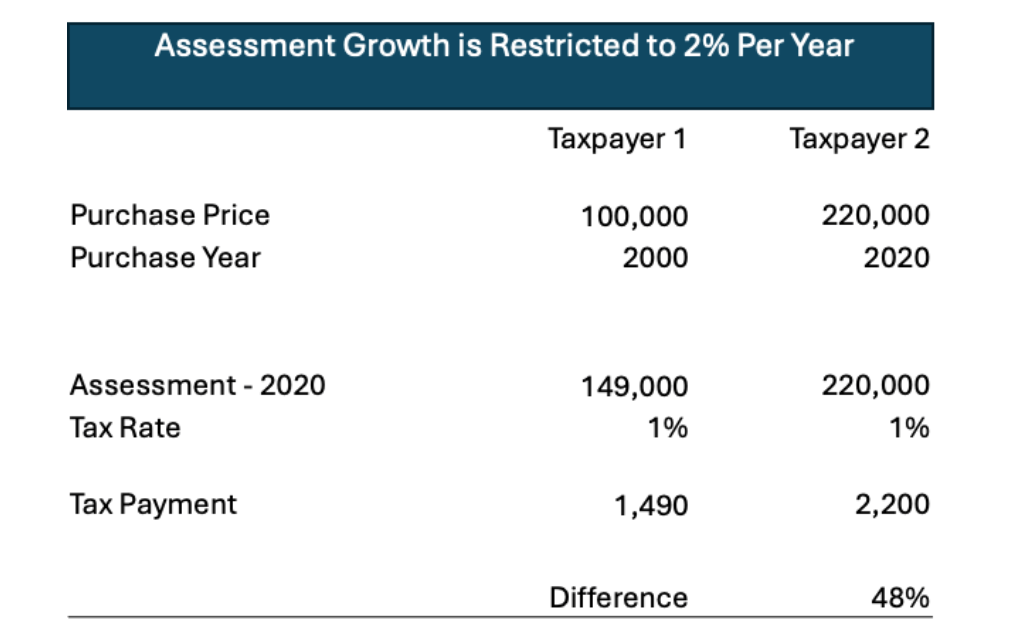

Example: Assessments limited at time of purchase

Assessment limits often come into effect when the owner purchases a property. This leads to significant inequity when a long-term owner has enjoyed the benefits of the limit, and a new owner pays taxes based on the current market value.

In the example below, Taxpayer 1 purchased a property in 2000 for $100,000 and the assessment has been capped at this level ever since. Taxpayer 2 purchased a comparable home next door in 2020. Over the 20 ensuing years, the market value for homes in the area increased by an average of 4 percent a year (comparable to national averages for this period), so Taxpayer 2 paid $220,000 for the home. While the tax rate of 1 percent is the same for both taxpayers, the difference in assessment for the properties results in a tax bill of $2,190 for Taxpayer 2, more than twice the $1,000 tax bill for Taxpayer 1. Both homes have similar market values and enjoy the same access to public services, but Taxpayer 2 pays significantly more in taxes.

Even when assessments are allowed to grow by a restricted amount, inequity persists. In the example above, if the assessment for Taxpayer 1 were allowed to grow 2 percent per year—a rate that is still less than the rate of market value increase—the bill for Taxpayer 2 would still be 50 percent higher.

Even when assessments are allowed to grow by a restricted amount, inequity persists. In the example above, if the assessment for Taxpayer 1 were allowed to grow 2 percent per year—a rate that is still less than the rate of market value increase—the bill for Taxpayer 2 would still be 50 percent higher.

The longer an assessment limit is in place, the higher the level of inequity.

Assessment limits often shift the tax burden toward poorer taxpayers and neighborhoods.

Cross-neighborhood disparities are often associated with vertical inequity. Vertical equity reflects the distribution of the tax burden among different housing price levels. With vertical equity, high-value properties are assessed at the same level as low-value properties, with respect to the market.

If assessment growth is restricted by an assessment limit, lower-valued properties that appreciate less in value are assessed at a higher level than more valuable properties. This is a regressive property tax distribution where vertical inequity exists.

New York City provides a real-world example of how an assessment limit produces this regressive pattern. The chart below shows the effective tax rates of properties at different price levels in New York City, which has had an assessment limit in place since 1981. The chart illustrates a regressive pattern, with lower-priced properties paying a higher effective tax rate than higher-priced properties. In fact, the lowest-priced properties pay an effective tax rate of 1.26 percent, more than twice the rate of 0.51 percent for the highest-priced properties, which have values in excess of $10 million.

Because the owners of lower-valued properties are paying a higher tax rate, they are effectively providing a subsidy to owners of more expensive properties. This inequity is often an unintended consequence of an assessment limit.

Assessment limits can result in many taxpayers paying more in property tax than if there were no limit.

While the intent of policymakers imposing assessment limits is to lower property tax bills, studies have shown that it is possible for most taxpayers to pay more under an assessment limit than they would without a limit.

- A 2006 study by the Minnesota Department of Revenue found the state’s assessment limit resulted in 78 percent of properties paying more than they would without a limit.

- A 2005 Idaho study found that while 86 percent of the residential parcels in one county would have their assessments reduced by a limit, 60 percent of the parcels would pay more than they would without a limit.

- A 2018 study by the NYC Independent Budget Office found that removing its longstanding assessment limit and returning to market-based assessments would result in more than 70 percent of residential homestead properties (499,000 out of 700,000) paying less in property taxes, with a median savings of $1,100.

The example below demonstrates how this can occur.

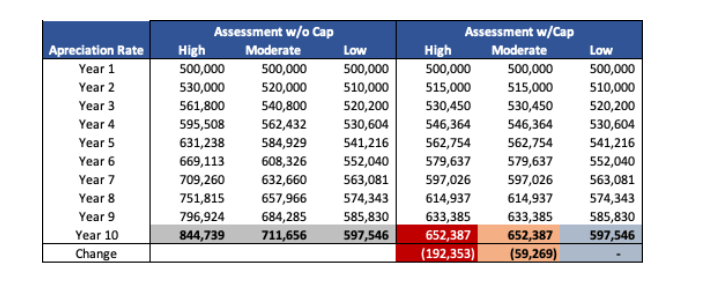

Assume there are three homes in different neighborhoods, all with a value of $500,000 in Year 1, and that an assessment limit restricts the growth in assessments to 3 percent per year. In this example, three neighborhoods experience three different levels of market appreciation:

- 6 percent per year in the high appreciation neighborhood

- 4 percent per year in the moderate appreciation neighborhood

- 2 percent per year in the low appreciation neighborhood

In the example, the amount of tax revenue is held constant, so the 1 percent tax rate used by the community in the first year drops to compensate for the increase in assessments.

The table above shows how assessments for the three properties would change over a 10-year period without a limit, and how they would change with a 3 percent annual limit on assessment increases. The high appreciation property benefits the most under the assessment limit; by the final year, the limit has reduced its assessment by over $190,000. The home with moderate appreciation also benefits, but to a lesser degree. After ten years, its assessment has been reduced by just under $60,000. The appraised value of the low-appreciation home is never affected by the assessment limit. Over ten years, the value of the home with high appreciation increased at three times the rate of the low appreciation home, but its assessment is only 9 percent higher than the low-appreciation home.

The impact on the taxes paid by each homeowner is also unexpected. Not surprisingly, the limit reduces taxes on the high appreciation home each year, with cumulative savings of $3,663 after ten years. The low appreciation home that did not benefit from the limit pays more each year to offset the savings of the high appreciation home, and over the ten years has paid an additional $2,792 in taxes because of the limit. More surprising is the effect of the limit on the moderate appreciation home. Despite having its assessment lowered each year by the limit, it still pays nearly $1,000 more in taxes, again to help subsidize the savings enjoyed by the high appreciation home. The moderate appreciation taxpayers likely believed they were paying less under the assessment limit, but in fact were paying more. This is one of the more deceptive features of assessment limits.

This example demonstrates how assessment limits can actually increase taxes for most homeowners, with slowly appreciating homes subsidizing the homes whose values have appreciated the most. Here, after ten years the high appreciation home is worth 19 percent more than the moderate appreciation home and 41 percent more than the home of low appreciation, but their higher taxes are subsidizing the tax savings of high appreciation homes. Asking owners with stagnant home values to subsidize owners whose home value has increased significantly is illogical and is another inequitable outcome of assessment limits.

Assessment limits create a “lock-in” effect that reduces mobility and competitiveness

Assessment limits can also reduce the efficiency of real estate markets and local economies when taxpayers are reluctant to move to a new property with a new assessment.

- A growing family in a starter home may choose not to trade up to a larger home, reducing the inventory of starter homes for families with fewer financial resources. At the same time, a couple who no longer require a larger house may be reluctant to downsize if that would increase their property tax liability.

- A homeowner may choose not to accept a job in a new location in order to avoid a larger tax bill on a new home.

- Businesses may also experience this “lock-in effect,” not moving to a larger facility, or one closer to their market, to preserve benefits accrued under an assessment limit.

- Long-tenured businesses may have a competitive advantage over new businesses, inhibiting competitiveness and economic growth.

- Residents with significant tax benefits may increase the demand for public services if they are insulated from the associated tax cost.

The California Legislative Analyst’s Office studied changes in ownership after enactment of the Proposition 13 assessment limit, finding that before enactment 16 percent of properties were sold in one year; thirty-five years later, that share had declined to only five percent. [California Legislative Analyst’s Office, Common Claims About Proposition 13, page 11 (2016)]

This chart illustrates the potential power of the lock-in effect created by assessment limits, comparing property tax payments for a newly purchased home and a home of equal value held for the average ownership period in cities with assessment limits. For example, taxes on a recently purchased median-value home in Tampa, Florida will be over two and a half times those for a home of equal value owned for the average duration. This situation can create an economic barrier to new homeowners and discourage existing homeowners from moving or upgrading to a larger, smaller, or more appropriate home.

Assessment limits are difficult to repeal once implemented, but experience shows a gradual phase-out can work.

Despite these drawbacks, assessment limits are very difficult to repeal once they are implemented. Over time, owners benefiting from assessment limits can enjoy deep discounts on their property tax bills. Any significant tax increase from removing or reducing the limit becomes extremely difficult politically, even if the majority of taxpayers would end up paying less after repeal. Owners are unlikely to become politically active because of lower taxes, stable taxes, or a slight tax increase, but dramatic tax increases are sure to bring calls for relief. Ironically, this has been a major reason for adoption of assessment limits, ever since an 80 percent increase in California house prices from 1975 to 1978 led to enactment of Proposition 13 (Fisher, Bristle, and Prasad 2010).

In this situation, a graduated phase-out is a realistic approach to remedying the drawbacks of assessment limits. A Lincoln Institute of Land Policy working paper provides guidance on how a gradual repeal of an assessment limit might be implemented. Minnesota had an assessment limit for four classes of property, including residential and agricultural homesteads, from 1973 to 1979, and again from 1993 to 2008. In 2001 the legislature established a six-year phase-out period, which was extended in 2005 for an additional two years (Karen Baker and Steve Hinze, Minnesota House Research Short Subjects Limited Market Value). A 7% assessment limit for homestead property was put in place in 2004 in Cook County, Illinois which includes the city of Chicago; it was phased out over a number of years and replaced by an increased homestead exemption in 2013.

Circuit breakers are particularly effective at limiting the impact of increasing taxes on those who do not have the income available to pay.

Property tax circuit breaker programs provide targeted property tax relief to households with the heaviest tax burdens relative to their incomes. Like the circuit breaker in an electrical panel, property tax circuit breakers are “tripped” when property taxes exceed a set threshold percentage of income. The circuit breaker offsets property tax payments above that level.

Homestead exemptions and credits are the most common type of property tax relief usually available for all owner-occupied primary residences of taxpayers, although they can be limited to select groups of homeowners such as seniors.

Flat dollar homestead exemptions, where the exemption amount is the same regardless of the value of the property, are preferable because they target larger relative tax savings to lower- and moderate-priced properties.

Tax Deferral programs directly address the problems faced by cash-strapped taxpayers (usually older adults) with significant equity in their homes to pay current property taxes.

They allow homeowners to use an otherwise illiquid asset—their home equity—to satisfy their property tax obligations. Since the tax is repaid out of the proceeds when the property is sold or transferred, deferrals have no long-term cost to other taxpayers.

Monthly Payments are typically structured as prepayment programs that allow payments to accumulate in an escrow account, which is then used to pay the annual or biannual tax bill.

The property tax is unlike most other bills or taxes in that it is paid in a few large, lump sum amounts each year. Providing taxpayers with a monthly payment option avoids large lump sum payments and makes property taxes more affordable.

Truth in Taxation is designed to avoid “silent” tax increases that occur when rising values produce higher tax bills without any change in the official tax rate.

Truth in Taxation programs require that any increase in property tax revenues due to increases in assessments follow the same procedures required for an increase in the tax rate. This may involve advertisements, public hearings, and mailed individual notices identifying the impact on individual tax bills. Truth in Taxation can limit property tax increases during periods of rising home values by encouraging more responsive tax rate setting while avoiding the unintended consequences associated with other types of tax limits.